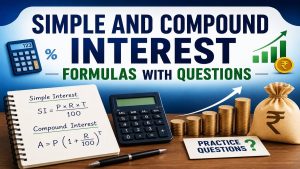

Simple and Compound Interest Formulas with Questions

Interest is one of the most significant ideas in maths and financial calculations. It is very common in banking, loan applications, investments, saving account and competitive exams. Simple Interest and Compound Interest make it easier to find out how much more is earned and/or paid on a principal during the period of time. These Interest … Read more

Read More

Student Discussion

Be the first to comment.

ADD NEW COMMENT